Author: Mario Ortez, PhD Candidate, Purdue University Department of Agricultural Economics. Learn more about Mario from his past writings on Consumer Corner Thoughts on Value, Cost and Price and In Favor of Differentiation.

Though some manufacturing businesses assemble pieces together to achieve a final product, the beef manufacturing industry (along with other livestock industries, recall chicken wings come from chickens) does the exact opposite. They dissemble a carcass into different cuts. More specifically, the carcass is broken down into different primals, and primals are broken down into different cuts. The biology of cattle is such that beef cuts have very significant differences in characteristics that translate into different attributes, like tenderness, juiciness, flavor and appearance. Where specific beef cuts end up in the market is often heavily influenced by those biological characteristics (plus other social, cultural and preference aspects), which in turn may influence where consumers want to eat them.

Supermarkets, restaurants, hotels, further processors, distributors and export markets are the most prominent distribution channels of fresh beef in the United States. Restaurants have preferences for certain beef cuts, and such preferences are likely different than those of supermarkets. Even more, some beef cuts may heavily rely on export markets for their distribution. Understanding such complex but exciting relationships is a first step into the world of beef.

Among agricultural economists, price relationships across different segments of the beef supply chain have long been of interest. For example, the price difference between wholesale beef (the price paid to the packing plants) and retail beef (the price paid to supermarkets) have allowed economists and stakeholders to understand the structure of the beef supply chain and how this structure may change over time.

I recently proposed a new way to study beef prices by looking at the price relationships of different beef cuts within each segment of the supply chain. I believe the intricacies that are particular to different beef cuts, stemming from their individual characteristics and extending to their final usage, may shed light on important economic happenings in this industry. Further, the price relationship of beef cuts within a segment of the supply chain — let’s say wholesale — and its change overtime may affect profits on the beef packer side and also influence the type of cuts a supermarket will feature at the store. This influence may ultimately influence what the final consumer chooses to purchase.

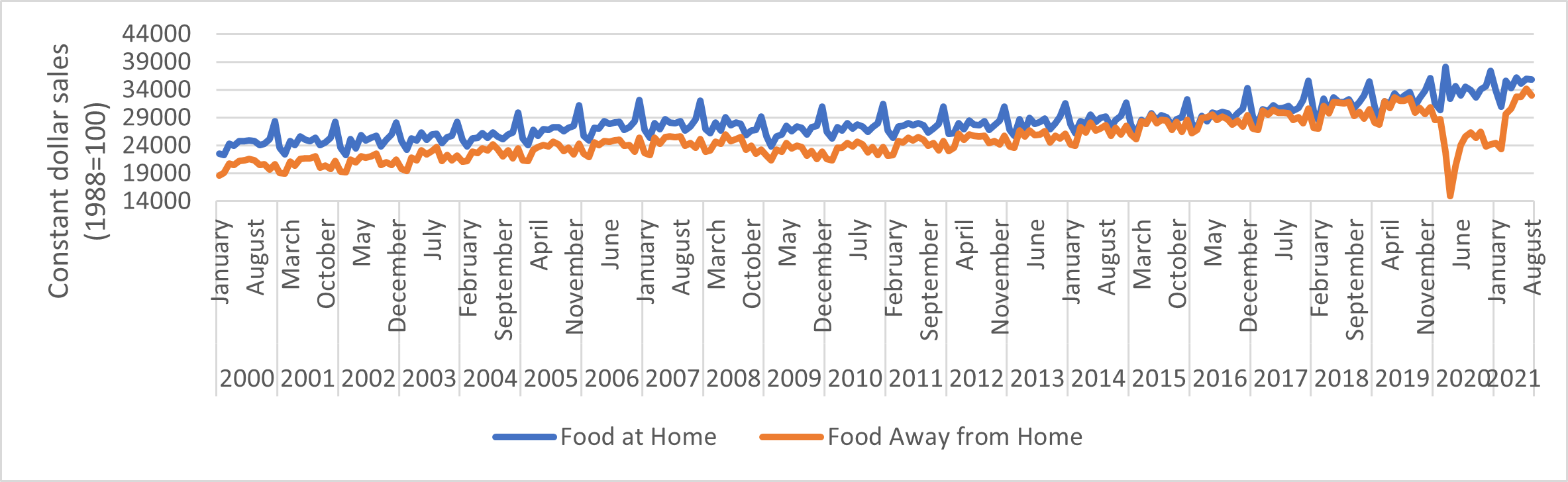

Of interest in my ongoing research in collaboration with Drs. Nathanael Thompson and Nicole Olynk Widmar is the effect of a localized (within a segment of the supply chain) shock into beef markets, namely restaurant closures. We know that filet mignon, made from wholesale tenderloin, is traditionally purchased at restaurants (Gibson, 2020) and is the most frequently menued steak by full-service restaurants (Daley, 2018), making it the largest dollar generator in the beef category of the food service sector (Pawlak & Napier, 2019). This makes tenderloins heavily rely on restaurants for distribution to consumers, more so than other beef cuts, say NY strips or chuck rolls (used for roasts), which are popular in supermarket specials. We also know restaurants closed in 2020 due to COVID-19 and have been reopening since then, inducing a decrease in food away from home spending not seen in the last two decades, not even during the 2008 financial crisis (See Figure 1).

Figure 1. Food at home versus food away from home

(USDA ERS, 2021)

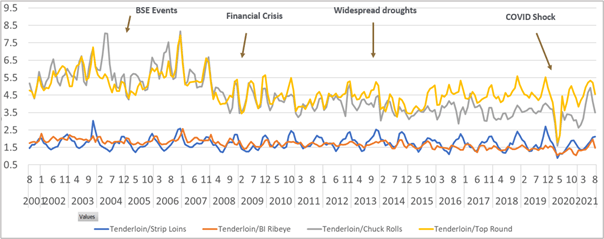

We considered that this is a scenario where a market disruption (restaurant closures) may have a disproportionally negative effect on some beef cuts (like tenderloins) more than on others. To study this hypothesis, we built a wholesale price ratio of tenderloins over other beef cuts to see how they have behaved over time and how they behaved in light of restaurant closures and COVID-19 induced disruptions overall (see Figure 2).

Source: USDA, Agricultural Marketing Service 2021

Take the tenderloin/chuck roll price ratio (gray line) as an interpretation example: Figure 2 shows that in August of 2021, tenderloins traded for 3.5 times the price of chuck rolls, while at the heights of restaurant closures in 2020, this ratio collapsed down to almost 1.5 times. More generally, Figure 2 shows that though there have been severe shocks in the beef markets over the past two decades, including BSE (bovine spongiform encephalopathy) events, financial crisis and widespread droughts, none of them have had such a severe effect on the price relationship of tenderloins and other beef cuts. This lends support to our hypothesis that the novelty of the localized shock of restaurant closures had a disproportional effect on some beef cuts.

There is great complexity in the combination of factors that ultimately led to this highly unusual price relationship behavior of beef cuts, but we can infer a few things from the inability of the relationship to remain somewhat stable during 2020. One is that retail, processors or even export markets (which are food services’ alternative distribution channels) were not substantially able to absorb the supply of tenderloins that usually go to food service. Another possibility is that consumers were not willing or able to purchase tenderloins in retail settings, inducing supermarkets not to seek them in the wholesale markets. Many other reasons could have played a role, but in any regards, as we approach the Thanksgiving and Christmas holidays this year, it appears tenderloins in 2021 have recuperated their proportional pricing to other beef cuts, which may not be great news for those of us who may have taken advantage of their unusually relative lower prices in 2020.

ConsumerCorner.2021.Letter.38