Purdue Agribusiness Review, Volume 1, Issue 1

The paradox of confident caution

On paper, your company might look ready for the future. You have an artificial intelligence (AI) strategy. Senior leaders have attended vendor demos, approved pilot projects and invested in dashboards that promise better forecasts and tighter coordination. Your organization talks fluently about machine learning, data-driven decision-making and digital transformation. Yet, months later, very little has changed. Core decisions are still made the same way. Frontline managers quietly override algorithmic recommendations. Data lives in shadow systems that don’t quite connect. The pilots continue, but they never quite become part of how the business actually runs.

This pattern is not unusual. In fact, it is increasingly the norm. Our 2025 survey of 281 agribusiness supply-chain participants across the United States reveals a striking paradox. Agribusiness leaders are highly confident in the potential of Industry 4.0 technologies, particularly artificial intelligence. Roughly 72% of respondents believe AI is likely to improve productivity, and nearly 80% expect it to strengthen resilience, helping firms respond to disruptions and manage risk more effectively. Expectations for the Internet of Things (IoT) follow a similar, if slightly more modest, pattern.

But confidence has not translated into action. Only 5.5% of respondents report that AI is well or fully integrated into their supply-chain operations. The majority report no use, no integration or only minimal experimentation. In many organizations, AI exists at the periphery. More broadly, Industry 4.0 (AI, IoT and Blockchain) is visible enough to signal progress, but not deeply embedded enough to change who decides, how decisions are made or who is held accountable. The result is a familiar but frustrating puzzle. Agribusiness believes in AI, invests in AI and talks about AI, yet largely stops short of using it effectively. Often, this gap between belief and action is a change management problem.

Why Industry 4.0 feels different in agribusiness

To understand the gap, it helps to clarify what these technologies actually do and where their value truly comes from. In a digitally integrated agribusiness ecosystem, AI serves as the decision-making engine, transforming data into forecasts, recommendations and automated actions. IoT functions as a sensory network, capturing real-time data from fields, equipment, inventory and logistics. Blockchain provides a secure ledger, ensuring traceability, data integrity and shared trust across partners. Together, IoT generates the signals, blockchain protects and authenticates them, and AI turns them into operational intelligence.

And to be fair, agribusiness is not an easy environment in which to deploy Industry 4.0 technologies. Production is shaped by biological systems that resist standardization and generate outcomes no algorithm can fully control. Weather, disease pressure and yield variability inject uncertainty that even the best models can only partially tame. Margins are often thin, which raises the stakes of experimentation. A failed pilot in a consumer-tech firm may be an inconvenience; in agriculture, it can jeopardize an entire season’s profitability. Supply chains are also fragmented, stretching across producers, input suppliers, processors, distributors and retailers that vary widely in size, sophistication and digital readiness. Information moves unevenly, and incentives are rarely aligned.

In many agricultural segments, dispersed market power makes it difficult to impose the common data protocols and operating standards that blockchain technologies depend on. Because their value is inherently collective, adoption requires coordination that fragmented markets struggle to achieve. Then there is the issue of data. Unlike many industries, agribusiness data is deeply entangled with questions of ownership, control and trust. Farmers (reasonably) worry about who benefits from the data they generate. Firms hesitate to share information that could weaken their bargaining position or expose proprietary practices. These concerns complicate integration and slow collective learning.

Taken together, these constraints help explain why agribusiness leaders approach Industry 4.0 with caution. They also explain why simple analogies to manufacturing or retail digitalization often fall flat, but they do not explain why so many firms stop at pilots. Biological uncertainty does not require organizations to leave decision rights unchanged. Thin margins do not require indefinite experimentation without escalation. Fragmentation and data concerns make coordination harder but not impossible. In fact, these conditions are precisely where better coordination, clearer governance and faster learning should matter most.

The persistence of pilot projects, dashboards that inform but do not decide and tools that never quite reach the operational core points to a different constraint. The bottleneck likely has nothing to do with technological feasibility or employee sophistication. More often than not, the challenge lies in the managerial willingness to redesign how decisions are made, how risk is shared and how authority shifts as new capabilities emerge. Even though the technologies might be suitable for industry needs, Industry 4.0 feels different in agribusiness because adopting them forces choices about organization, control and commitment that many firms are reluctant to confront.

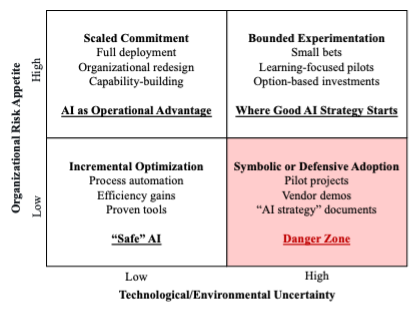

Introducing the Matrix: Commitment under uncertainty

To make sense of what we’re seeing, it helps to shift the conversation away from “adoption” and toward a more practical question: How much is a firm willing to commit when the technology and the environment around it are still uncertain? Figure 1 organizes those choices along two dimensions. The horizontal axis captures technological and environmental uncertainty. How unclear are the performance, integration requirements, standards and downstream implications of the technology still in your context? The vertical axis captures the firm’s organizational risk appetite. How willing is your firm to absorb short-term disruption before the payoff is fully proven? This could include retraining people, redesigning workflows, reallocating decision rights and building new capabilities.

This framework is not intended to rank firms as “advanced” or “behind.” The goal here is just to describe the strategic posture firms take while Industry 4.0 is still evolving. Two firms can have access to the same tools and make very different choices about how deeply to embed them, how broadly to scale them and how quickly to reorganize around them. That posture tends to fall into four patterns:

- Incremental optimization (low uncertainty, low risk appetite): adopting proven tools for local efficiency gains without major organizational disruption.

- Scaled commitment (low uncertainty, high risk appetite): embedding technologies deeply and redesigning operations to capture sustained advantage.

- Bounded experimentation (high uncertainty, high risk appetite): running disciplined pilots designed to generate learning and preserve future options.

- Symbolic or defensive adoption (high uncertainty, low risk appetite): investing in visible initiatives without changing the organization enough to realize value.

In the sections that follow, we use survey evidence to show where agribusiness firms are actually landing in this matrix and why the most common position is also the most dangerous one.

The Empirical Center of Gravity: The “danger zone”

When we map agribusiness behavior onto this matrix, the “danger zone” dominates. Rather than entirely rejecting Industry 4.0 or pursuing some bold transformation, firms opt for more costly ambiguity. Nearly 38% of survey respondents report that their firms use none of the listed Industry 4.0 technologies or are unsure whether they are used at all. At the same time, more than two-thirds say they are actively exploring or considering adoption. Interest is widespread. Action, however, remains tentative.

Even among firms that have adopted AI, IoT or blockchain, the depth of integration is shallow. Across all three technologies, the most common response is minimal to moderate integration via pilot projects, limited use cases or isolated applications. Advanced integration is rare. Only 5.5% of respondents report AI as well or fully integrated into their supply-chain operations. The figures are even lower for blockchain and only modestly higher for IoT. This pattern reveals something important. Agribusiness firms are not hostile to technology. They’re mostly aware of its potential, and they’re not standing still. Unfortunately, our data suggest that they’re caught in a mode of symbolic or defensive adoption, characterized by visible activity without organizational commitment. In the matrix, this is the danger zone: high uncertainty combined with a low willingness to redesign how the organization works.

But the “danger zone” is not equally intense across technologies.

IoT often represents the least disruptive entry point. Sensors expand visibility, tracking conditions, inventory or equipment performance, without immediately altering who holds decision authority. Data gathering can be layered onto existing workflows with relatively limited organizational redesign. The challenge is operational, but not necessarily political. Blockchain presents a different hurdle. Its core friction lies in governance: data sovereignty, verification protocols, and inter-firm coordination. Adoption depends less on redesigning internal judgment and more on aligning incentives at the executive level.

AI is different. It does more than simply observe the system. It also recommends, prioritizes and automates decisions, making the “danger zone” more acute. Integrating AI into core operations often requires reassigning decision rights, retraining employees, redefining accountability and accepting short-term performance volatility as humans learn to work alongside algorithms. It has the potential to change not just workflows but the authority of the workload itself. This distinction helps explain why AI generates the highest expectations in our data but with the deepest integration gap.

From a managerial perspective, the logic is understandable. Pilot projects carry relatively little downside. They can be funded modestly, framed as learning exercises and discontinued quietly if they disappoint. They can also serve as a faux signal of progress to boards, partners and customers without forcing hard conversations about who now has authority, which workflows must change, or how accountability should shift when algorithms begin to influence decisions.

By contrast, deeper integration carries perceived risks that loom much larger. Embedding AI into core operations often requires reassigning decision rights, retraining staff, breaking down data silos and accepting short-term performance volatility. These are organizational hurdles rooted in a fundamental question about how your organization learns. And unlike pilots, they create visible winners and losers inside the firm. The result is a steady accumulation of experiments that inform but do not decide, tools that advise but do not govern, and dashboards that coexist with legacy decision processes, rather than replacing them altogether. Over time, firms become busy talking about AI while remaining fundamentally unchanged by it. That is why the danger zone persists. It offers the comfort of motion without the discomfort of commitment.

What firms think is holding them back, but what actually is

When agribusiness leaders explain why Industry 4.0 initiatives stall, they tend to point to a familiar set of barriers. In our survey, the most commonly cited constraints are lack of technical expertise, uncertainty about the benefits and high implementation costs. By contrast, regulatory and compliance uncertainty ranks among the lowest concerns. At first glance, these appear to be technical or economic problems. Firms lack the right skills. The return on investment is unclear. The upfront costs feel hard to justify. Those explanations are not wrong, but they are incomplete. Read more closely, and these barriers are better understood as signals of organizational unreadiness.

A lack of technical expertise often reflects deeper questions about who is responsible for integrating new tools into existing workflows and how new analytical capabilities fit alongside established roles. Uncertainty about benefits frequently stems from the absence of clear decision rights: if no one knows who will act on an algorithm’s output, it is difficult to value that output in advance. High implementation costs are magnified when data are fragmented, systems are poorly aligned, and learning cannot be shared across the organization.

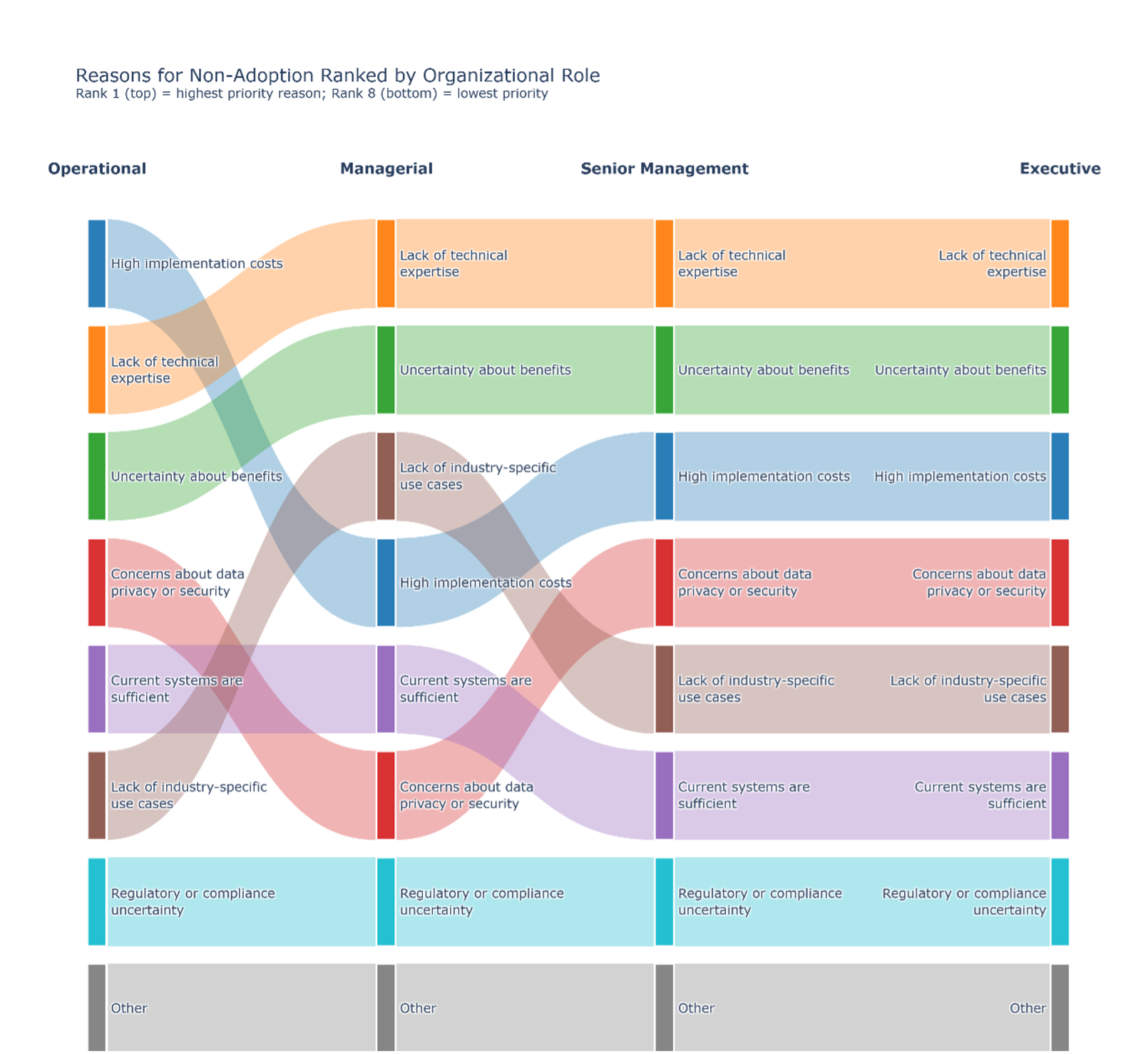

Figure 2 demonstrates the execution gap. The sample comprises 72 executives, 44 senior managers, 30 managerial-level respondents and 18 operational respondents across production, manufacturing, wholesale, distribution, retail and agricultural service segments of the U.S. supply chain. Frontline actors rank high implementation costs 281 as the foremost obstacle. Yet above the managerial tier, cost recedes and is replaced by lack of technical expertise as the dominant barrier. In other words, what appears as “cost” on the ground is perceived as “competence” at the top. Each level attributes the bottleneck to the other. Operations experience resource constraints while managers diagnose capability gaps. This divergence signals the absence of a central coordinating logic for adoption, indicating a breakdown in vertical communication. Responsibilities are unclear, ownership is diffuse, and there is no shared pathway for translating experimentation into organizational change. As a result, adoption stalls because the organization has not yet learned who should act and where the new tools are most effective.

The open-ended responses make this dynamic even clearer. Respondents point to data silos that prevent AI systems from drawing on complete or consistent information. Others emphasize data sovereignty, noting the need for tools that “add value while maintaining control over data.” Concerns about who can access data, how it can be used and who ultimately benefits appear repeatedly. Surprisingly, none of these concerns represents the open-ended question about whether the technology works. Instead, our respondents largely focused on governance concerns, reflecting unresolved questions about coordination, accountability and authority in digitally enabled organizations.

Survey question: In your own words, what do you think are the most important impediments to technology adoption in agriculture?

“Data silos – in order for AI to provide the benefits it is capable of, it needs wholistic and structured datasets, which few agribusinesses have given the data silos across input companies, retailers, OEMs, etc.”

“We need tools that are out of the box and that add value while maintaining data sovereignty.”

When firms frame these issues as purely technical or financial, the default response is to wait for better tools, clearer returns or lower costs. But waiting rarely resolves problems rooted in organizational design. Instead, it reinforces the very conditions that keep firms in the danger zone. By leaning into experimentation without escalation and learning without commitment, the new technology remains peripheral to how decisions are made. In other words, what firms think is holding them back is not what ultimately is holding them back.

Bounded experimentation is where good AI strategy starts

If the danger zone is defined by activity without commitment, the most promising alternative lies diagonally across the matrix. Good AI strategy begins where high uncertainty meets a strong willingness to learn and adapt. In our data, this posture is most evident among larger, vertically integrated and multinational agribusinesses. Respondents from these firms say they are more likely to adopt multiple Industry 4.0 technologies simultaneously, rather than experimenting with a single tool in isolation. They are also more likely to expect meaningful gains in both productivity and resilience from those investments. Larger, vertically integrated firms often possess greater market power and leverage across their supply chains. They can set operating requirements, establish shared data standards and require participation from suppliers and downstream partners in ways smaller or more fragmented firms cannot. That structural position makes it easier to scale technologies whose value depends on collective adoption, shared protocols and system-wide integration. What also distinguishes these firms is a different approach to commitment rather than a greater confidence in the technology itself. Instead of treating AI, IoT or blockchain as one-off initiatives or as symbols of modernity, they treat them as a portfolio of experiments designed to generate information about where value can actually be created.

This approach is best described as “bounded experimentation.” In this approach, successful firms define clear learning objectives for each pilot. They intentionally identify what uncertainty the project is meant to reduce and what decision it will inform if successful. They establish escalation paths in advance, specifying when an experiment should be expanded, integrated or shut down. Just as importantly, they are willing to both kill projects that do not deliver insight and to scale those that do. In this mode, pilots are fundamentally designed for organizational learning, with the goal of creating mechanisms for discovery. Each experiment is bounded in scope and cost but explicitly linked to future organizational choices. Over time, this allows firms to build confidence not just in technology but also in their ability to absorb and act on what it reveals. Seen this way, bounded experimentation reframes risk. Instead of worrying about making the wrong bet on a specific tool, this approach centers on learning quickly which capabilities are worth committing to and which are not.

When AI becomes an operational advantage

The top-left quadrant of the matrix represents scaled commitment under lower uncertainty. This is where Industry 4.0 begins to deliver operational advantage. It is also where very few agribusinesses currently reside. In our survey, only a small minority of firms report that AI, IoT or blockchain is well or fully integrated into their supply-chain operations. This scarcity is telling, suggesting that deep integration is a deliberate organizational choice that most firms have not yet made. The firms that reach this quadrant are no longer “adopting AI.” Scaled commitment involves redesigning workflows so that analytical outputs are embedded in routine decisions. It requires investing in capabilities such as data engineering, analytics literacy and cross-functional coordination to enable insights to travel across the organization. And it often requires an explicit managerial decision to define when algorithms should inform decisions and when they should make them. What these firms gain is not perfect foresight.

Value is rarely created through isolated optimization. A more accurate demand forecast in one part of the system means little if upstream production plans, logistics and procurement decisions remain disconnected. Firms that extract sustained value from Industry 4.0 focus instead on organizational learning and coordination across silos, using shared data and integrated systems to reduce friction and delay throughout the supply chain. This is why scaled commitment is both powerful and rare. At its best, this approach delivers benefits difficult for competitors to imitate, but only after firms confront the organizational changes many prefer to avoid. The payoff is all about leveraging your firm’s technological sophistication to create a supply chain that responds more coherently, more quickly, and more reliably when uncertainty inevitably arises.

Three questions that matter for agribusiness leaders

The key lesson here is not that agribusiness should move faster or slower with AI. Instead, the fundamental question is about organizational coordination itself. The difference between learning and stagnation, advantage and theater, often comes down to a small set of managerial choices that are easy to postpone and costly to avoid. Three questions are especially revealing.

1: Where does this technology change who decides, not just what we know?

The answer obviously depends on the technology. In the case of Artificial intelligence, it directly challenges decision rights. When AI generates forecasts, risk assessments or optimization recommendations, it implicitly asks whether authority should shift, from intuition to algorithm, from experience to analytics, from hierarchy to system-generated insight. If algorithms inform decisions but are not effectively integrated into your team’s workflow, their value will remain limited. Leaders should be explicit about which decisions are advisory, which are automated and require new forms of human judgment. Ambiguity here is rarely neutral. Without having those hard conversations, Industry 4.0 will be an expensive way to noisily preserve the status quo.

2: Are we experimenting to learn or to signal progress?

Pilots can serve two very different purposes. Some are designed to reduce uncertainty and inform future commitments. Others exist primarily to demonstrate activity to boards, customers or internal stakeholders. The distinction matters. Experiments that are not linked to clear learning objectives or escalation paths almost always stall, no matter how promising the technology.

3: What organizational risks are we avoiding and at what long-term cost?

Avoiding disruption feels prudent, especially in a volatile industry. But the world has never been more volatile. In the current macroeconomic climate, delaying decisions on data governance, capability development and coordination carries its own risks. Over time, firms that defer these choices may find that the competitors who might not necessarily be more advanced technologically but are more willing to reorganize can adapt faster when conditions change.

None of these questions can be answered by vendors, consultants or dashboards. They require leaders to confront trade-offs among control, commitment and trust within their own organizations. In that sense, Industry 4.0 forces agribusiness leaders to explicitly decide what kind of organization they are willing to run.

From technology adoption to organizational choice

Industry 4.0 is often sold as a way to tame uncertainty in agribusiness. Maybe we can get more accurate forecasts, coordinate workflows more efficiently or respond more quickly to shocks. That promise is appealing and not entirely misplaced; however, it is incomplete. Digital technologies will not eliminate biological risk, market volatility or supply-chain disruption. What they can do is change how organizations live with and learn from uncertainty.

Peter Drucker’s Theory of the Business reminds us that disruption is more about assumptions than it is about the tool itself. When an organization’s view of how the world works no longer matches reality, its structure and processes must evolve accordingly. Industry 4.0 represents precisely that kind of inflection point. Data moves faster. Insights surface earlier. Hierarchical authority is increasingly shaped by algorithms, creating the potential to dramatically change the business environment. For leaders, managing this shift will require confronting a set of uncomfortable questions. How quickly do you integrate new information into your decision-making process? How coherently do you act across silos? How confidently do you adapt when conditions shift?

Just like the rest of the modern business world, the Industry 4.0 paradox facing agribusiness today is the growing gap between enthusiasm and commitment. Many firms invest in AI, IoT and related technologies while stopping short of the organizational changes required to make them matter. The result is motion without momentum. Reframing digital transformation as a choice focused on organizational learning clarifies what is at stake. Industry 4.0 forces leaders to decide how much uncertainty they are willing to confront directly, and how much commitment they are willing to make before outcomes are fully known. Rather than the technology itself, it is the choice that determines whether experiments accumulate into advantage or fade into permanent pilots. In the end, competitive advantage in agribusiness does not come from being optimistic or cautious. It comes from matching commitment to uncertainty.

About the Center for Food and Agricultural Business

Founded in 1986, the Purdue University Center for Food and Agricultural Business is celebrating 40 years of working with the agribusiness industry to develop leaders and inform better decision-making. Housed within Purdue’s Department of Agricultural Economics, the center connects faculty expertise with the practical challenges facing food and agricultural companies.

The center delivers professional development programs, industry research and graduate education designed specifically for agribusiness professionals. Offerings include open-enrollment workshops, custom corporate training and the MS-MBA in Food and Agribusiness Management, a dual-degree program developed with industry for working professionals.

Through its research and publications – including the Purdue Agribusiness Review – the center shares industry insights from Purdue faculty and collaborators to help agribusiness leaders navigate change and make more informed strategic decisions.