Authors: Nicole Olynk Widmar, Associate Head and Professor, Purdue University, Department of Agricultural Economics, Dr. Courtney Bir, Department of Agricultural Economics, Oklahoma State University and Torrie Sheridan, Marketing Manager, Center for Food and Agricultural Business, Purdue University

Work environments are changing (whether we like it or not). Recall in 2020 Nicole suggested that we redefine the standards on what looking ‘awful’ means in order to avoid admitting that her then Zoom-chic self was really falling short of any pre-Covid-era standards. Then we revisited the 2022 fashion debate, including a look at spending on clothes and personal items from most recent data collection.

We already agreed that 2019 normal is never coming back, so it’s time to plan confidently (well, at least try) for the future instead of hoping for a return to the past.

Revisiting 2020 Comments: Time and Space Have Been Redefined

“I’ve benefited from a fluid workday schedule, however the lack of daily commute (as I am working from home with a small child out of school, aka, my coworker) has actually afforded me increased flexibility to get work done early in the morning, which is my preferred time. That aspect has been helpful (for me), although I acknowledge that I was a homebody beforehand and have always preferred my home office for writing compared to any other space. Others are struggling with this aspect significantly; those who work best in offices or coffee shops have been struggling for months (as have the offices and coffee shops in many cases).”

2022 Update: Wow, we were naïve thinking about short-term adjustments to workplaces in 2020, or potentially we were all emotionally maxed at the juggling and persistent strain of the unknown at that time. Either way, the changes to downtown locations, office spaces, real estate, and numerous economy sectors since have been intense and sweeping, and definitely not short-term. We thought the Great Resignation took place in 2021, but 2022 is delivering headlines like, “The Great Resignation is still in full swing”, so we are apparently not done yet with the massive changes to what our work lives look like (or home lives, for that matter — that elusive work-life balance is a persistent simultaneous discussion).

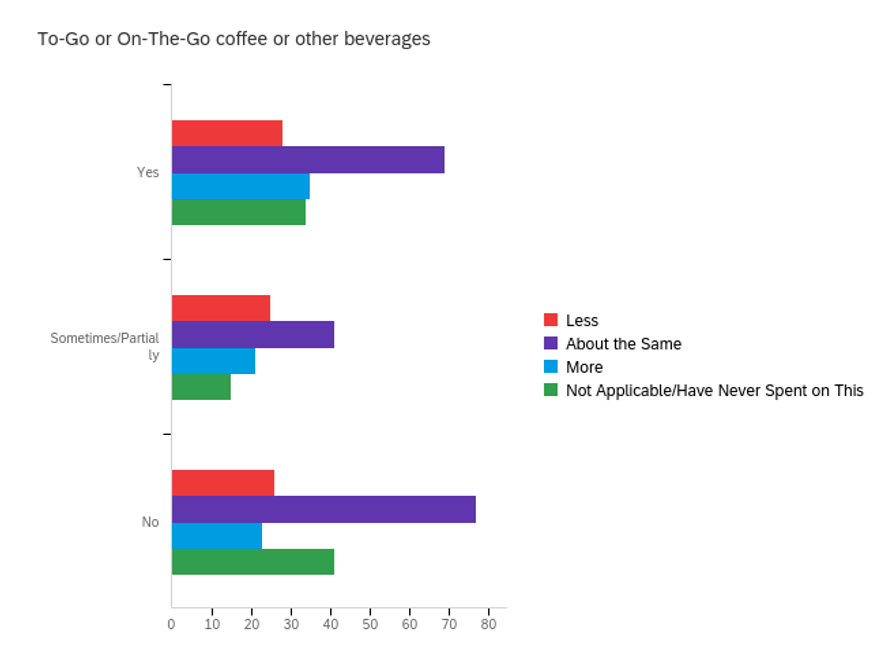

Last time, we talked about how personal spending habits (on clothes and such) changed in fall 2021 compared to pre-pandemic times. Now, we’ve broken responses out by whether one’s job can be performed remotely (responses included Yes, Sometimes/Partially, and No). Considering these elements associated with time and space, we were interested in spending on things like commutes, coffee on-the-go, etc. So, we’re looking at spending on to-go or on-the-go coffee and beverages in the fall of 2021 relative to pre-pandemic times, according to whether work could be performed remotely or not (or sometimes/partially).

Regardless of whether one’s work could be done remotely or not, the largest share of respondents for all three categories was that they were spending about the same as pre-pandemic. Dare we say, “normal spending”? For those who could work remotely, the second most popular response was that they were spending more in the fall of 2021 than pre-pandemic. In contrast, the second most popular (but only by a tiny margin) answer for those who could not work remotely was to spend less. So, if you can work remotely, you are more likely to spend the same or more, and if you cannot work remotely, then you are more likely to spend the same or less? Perhaps not what was expected, unless those who are remote more often crave outings or some social location? We can only hypothesize, but maybe we are all wanting to get out more, even if it isn’t to our physical work location.

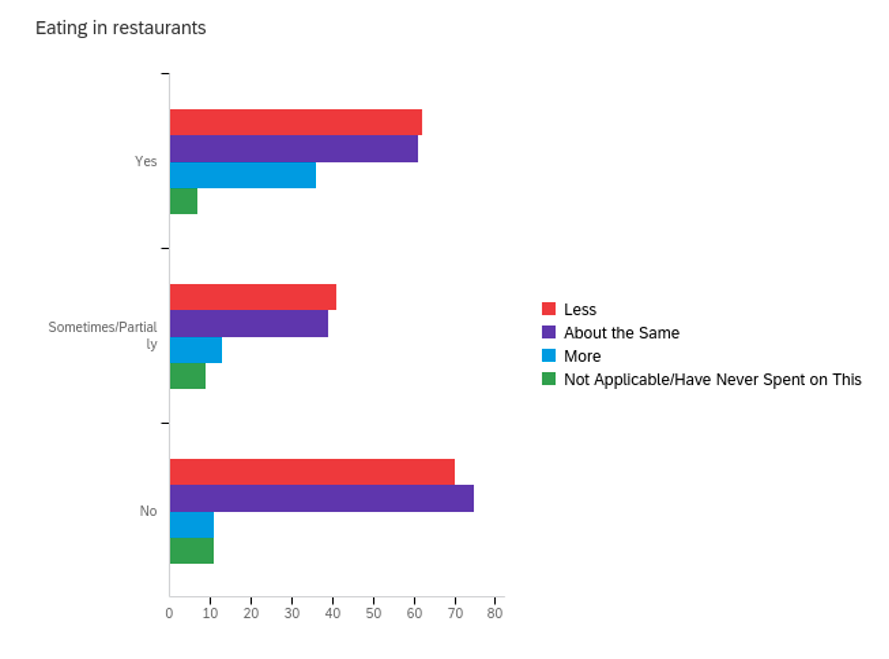

When considering eating in restaurants, most respondents reported spending less or about the same. A higher proportion of respondents who can work from home reported spending more on eating in restaurants than was seen for those who cannot work remotely or can do so only partially.

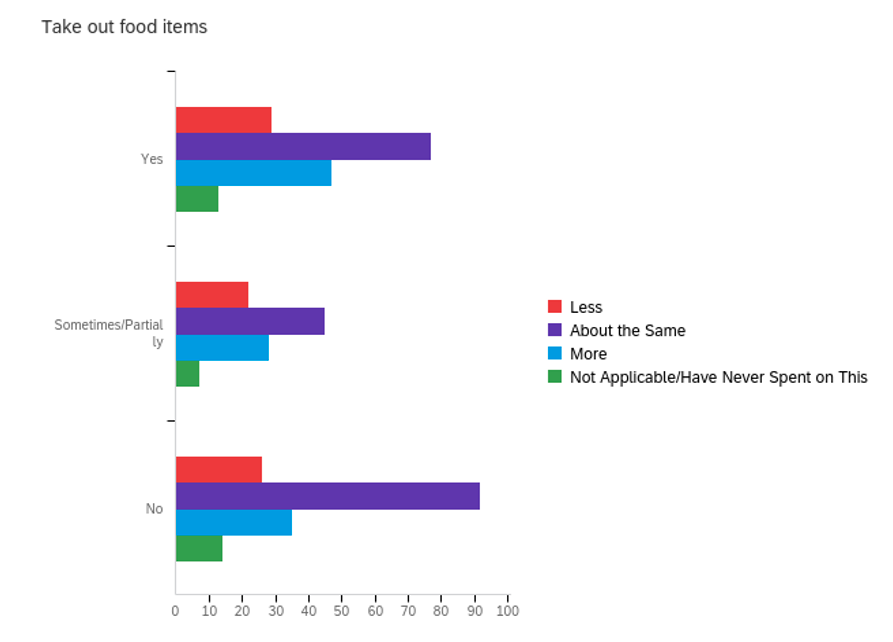

Spending on takeout food items was most commonly about the same, with the second most common answer being to have spent more in fall 2021 than pre-pandemic, regardless of work location. Given the massive changes in food at-home versus away-from-home versus the takeout food revolution that spurred during the pandemic (and continues for many of us!), the spending on takeout increasing is unsurprising. The real question may be, how long will it last?

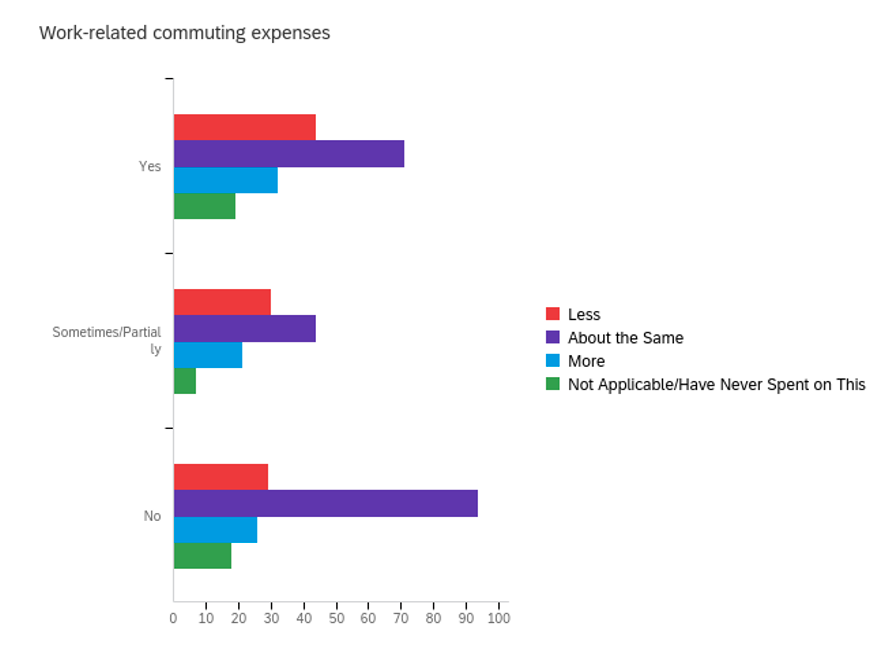

Unsurprisingly, working remotely lessened work-related commuting expenses, which was more pronounced for those who can work remotely than those who can do so only partially or not at all. Perhaps of interest is that while “about the same” was the most common answer for every category of worker, lessened spending was the second most common response, even amongst those who indicated they cannot work from home. Also of interest may be the not-insignificant proportion of respondents who indicated that they are spending more on commuting in the fall of 2021 than pre-pandemic. While we are unable to tease out why, one might question if some respondents may have taken new jobs during the pandemic or moved, leading to now higher commuting expenses as people return to physical work locations at least part of the time. This data was collected before the recent rise in gas prices, but perhaps commuting costs rose when markets for cars tightened and/or other factors associated with tightened supply chains and other factors took hold.

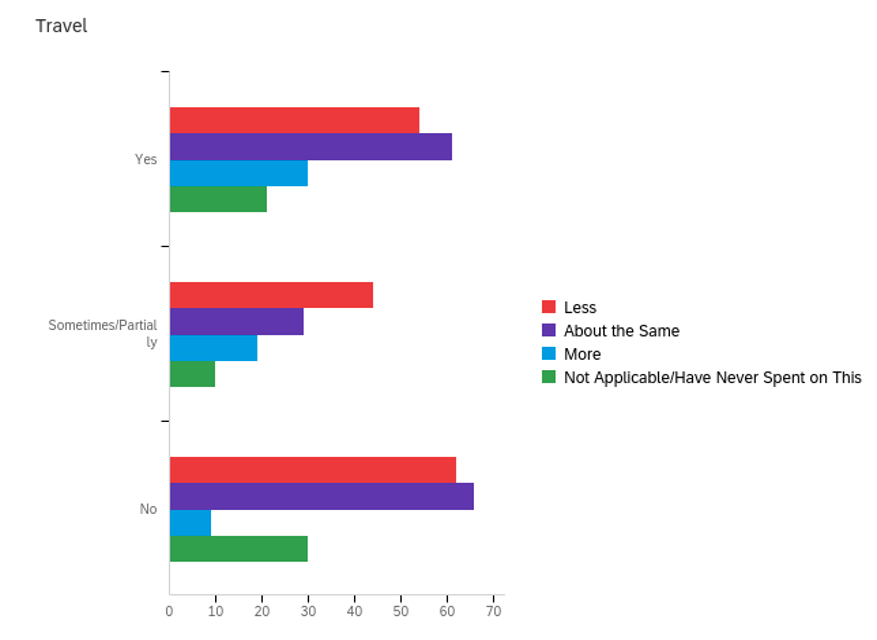

Travel spending is a particularly interesting expenditure category which has received a great deal of press and media attention throughout the pandemic. The most popular answer for those who can work remotely and those who cannot was to spend about the same in fall 2021 as they did pre-pandemic. In contrast, those who can work remotely sometimes or partially more often reported spending less. Likely these associations are unrelated to work modality, although it cannot be ruled out that work location flexibility may be related to one’s willingness or ability to travel (and thus their total travel expenditures).

Data analysis is still underway on this project, but thus far, we are confident in saying that the past several years have revealed that we (collectively, as a society) did not simply work-from-home for a bit and then return to our pre-2020 behaviors. What we seem to be facing now is a new negotiation in work-life balance (or integration?) that is much more holistic than we may have naively believed early on.

ConsumerCorner.2022.Letter.17